Executive Summary: Canal Istanbul has been promoted for years as a second Bosphorus, a global shipping route, and a future waterfront investment area. This article examines why that case does not stand up to serious scrutiny. The shipping revenue looks too weak, the construction cost too high, and the ecological, social, and legal risks too significant. For investors, the conclusion is simple: Canal Istanbul should not be treated as an active, guaranteed project, but as a political promise that remains commercially unproven and highly unlikely to be built as marketed.

The Sales Pitch: A New Bosphorus for Istanbul

Across parts of Istanbul’s real estate market, Canal Istanbul is still used as a powerful sales hook. Buyers are told they can buy near a future international waterway before prices rise. Some are shown maps, artist impressions, and phrases such as “new Bosphorus”, “future waterfront”, and “strategic investment area”.

It sounds persuasive, especially to overseas buyers who do not follow Turkish politics closely. Istanbul has a real history of infrastructure-led growth. The airport changed the north-west of the city. Bridges, highways, metro projects, and Urban Regeneration have all influenced land values in different districts.

But Canal Istanbul is different. The Bosphorus is a natural strait with centuries of history, established neighbourhoods, protected views, scarcity, and global recognition. Canal Istanbul would be an artificial shipping channel cut through land west of the city, connected to cargo movement, excavation, water management, logistics, and political risk. Calling Canal Istanbul, a new Bosphorus is not analysis. It is marketing.

What Canal Istanbul Would Actually Be

Canal Istanbul is a proposed 45km artificial waterway on Istanbul’s European side, running from Lake Küçükçekmece through the Sazlıdere area towards the Black Sea. The planned route would affect Küçükçekmece, Avcılar, Başakşehir, and Arnavutköy, with the largest section passing through Arnavutköy. It is planned to have a depth of about 20.75 metres and a base width of around 275 metres.

The plan has never been limited to water. If completed, the canal would effectively create an island on the European side. The project has also been linked to bridges, roads, logistics facilities, ports, a marina, and large new residential areas planned to house a population of up to 500,000 people.

If Canal Istanbul were only a maritime safety project, the real estate element would be secondary. Yet in practice, property development has always been central to how the project has been promoted, financed, and sold to the Turkish public. This is where investors should start asking harder questions.

First Problem: A Transport or Real Estate Project?

Supporters usually present Canal Istanbul as a solution to Bosphorus congestion. The Bosphorus is narrow, difficult to navigate, and dangerous when large tankers pass through the centre of Istanbul. That part of the argument is real. No serious person disputes that the Bosphorus carries risk.

The problem is what comes next. To justify Canal Istanbul as a commercial project, Turkey would need to prove four things:

- Enough ships would choose a paid artificial canal over the existing Turkish Straits.

- Canal revenue would cover construction, financing, maintenance, security, dredging, bridges, access roads, environmental works, and long-term operation.

- The fee would be high enough to make the project commercially valuable.

- The fee would not be so high that ships simply avoid the canal.

That is where the numbers start to fail.

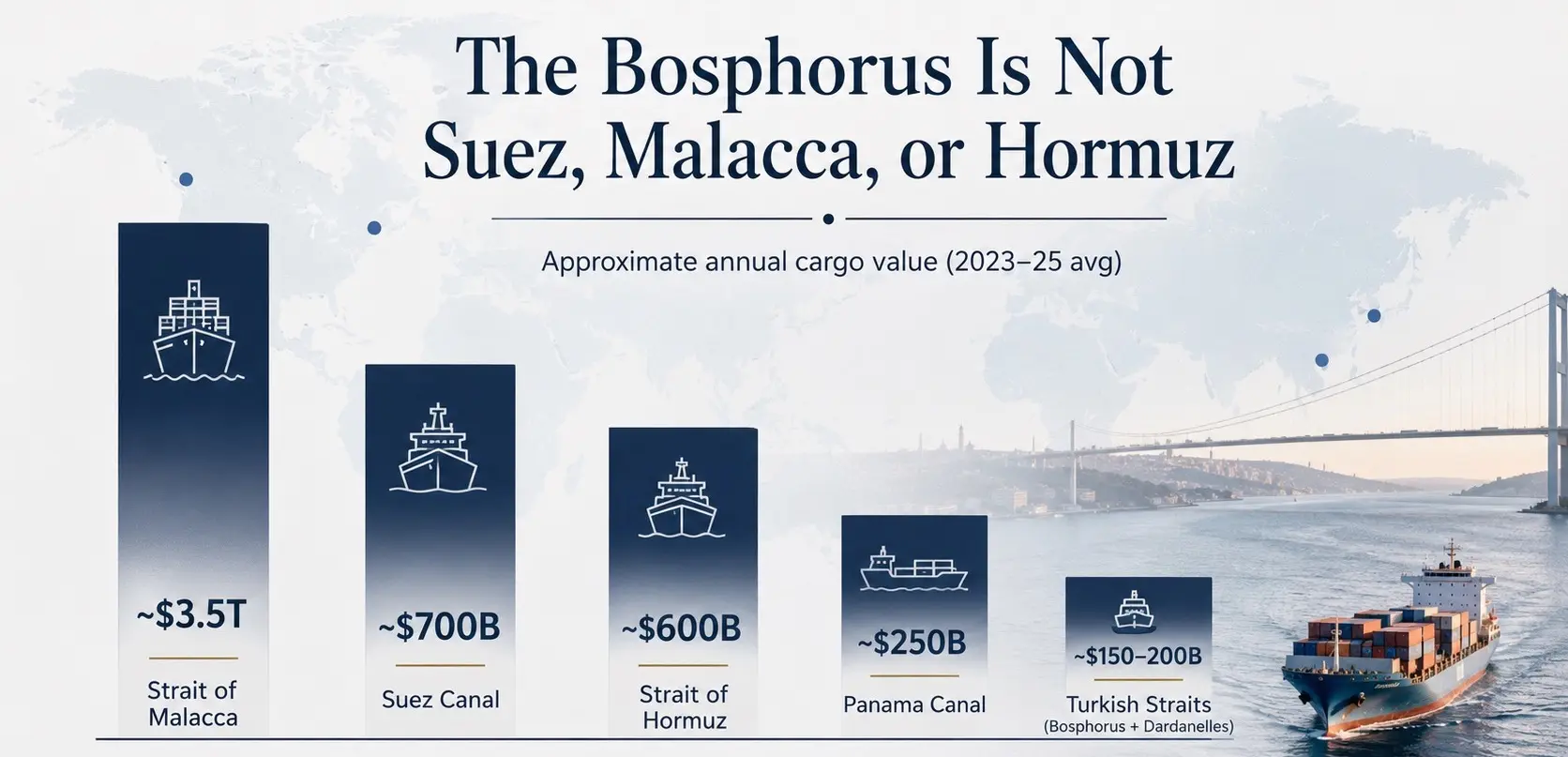

The Bosphorus Is Not Suez, Malacca, or Hormuz

The question is not only how many vessels pass through a route. The better question is what those vessels carry, how valuable the cargo is, whether ships have realistic alternatives, and whether the route saves enough time or distance to justify high fees. Using approximate annual cargo-value estimates, the Turkish Straits sit at the lower end of the world’s major waterways.

Waterway

Approximate Annual Cargo Value

Main Cargo Profile

Strait of Malacca / Singapore

Around $3.5 trillion USD

Oil, manufactured goods, containers, electronics

Suez Canal

Around $700 billion USD, higher in normal years

Containers, tankers, LNG, Asia-Europe trade

Strait of Hormuz

Around $600 billion USD

Crude oil and LNG

Panama Canal

Around $250 billion USD

Containers, dry bulk, LPG, vehicles

Turkish Straits

Around $150 to $200 billion USD

Bulk cargo, grain, coal, crude, general cargo

This does not mean the Turkish Straits are unimportant. They are vital for Black Sea access, Russian and Ukrainian trade, energy movement, grain routes, and regional security. But they are not Suez. They are not Malacca. They are not Hormuz.

The Turkish Straits carry a lot of tonnage, but much of that tonnage is lower-value bulk cargo. High toll power usually comes from high-value, time-sensitive cargo with limited alternatives. Bulk cargo is more cost sensitive. Margins are tighter. A high fee can quickly make a route unattractive.

The Revenue Problem: The Bosphorus Already Exists

Let us be deliberately generous to the Canal Istanbul argument. Assume the Turkish Straits carry cargo worth around $150 to $200 billion USD annually. Then assume Canal Istanbul somehow captures a large share of that movement. Even if the operator could charge the equivalent of 2% of cargo value, the theoretical revenue would be around $3 to $4 billion USD per year.

In 2025, more than 40,000 vessels passed through the Bosphorus. The issue is not whether the route is busy. It is whether enough ships would pay to use a new artificial canal when the natural Bosphorus still exists. From July 2026, Turkish Straits transit fees are due to rise to $6.70 per net ton for vessels passing without calling at a Turkish port. Yet projected revenue from the Bosphorus and Dardanelles together for July 2025 to June 2026 is still only $254 million USD.

Now compare that with the possible cost. Canal Istanbul would not only mean digging a channel. It would require bridges, roads, land acquisition, engineering works, dredging, environmental protection, security, financing, maintenance, and years of construction risk. A realistic all-in cost could easily reach $100 billion USD.

Revenue Assumption

Estimated Annual Revenue

Assumed All-In Project Cost

Simple Payback Before Running Costs

Current Turkish Straits fee scale

Around $254 million USD

Around $100 billion USD

Around 394 years

Aggressive 2% cargo-value charge

Around $4 billion USD

Around $100 billion USD

Around 25 years

The problem is clear. The current fee structure does not come close to supporting a project of this size. To make Canal Istanbul look financially viable, revenue would need to rise from hundreds of millions of dollars to several billions every year. Even then, the best-case payback period would still be around 25 years before running costs, financing costs, maintenance, dredging, environmental works, or future delays are included.

Canal-View Property Is Not Bosphorus Property

When the shipping case becomes difficult, supporters move to the second argument: even if the canal is expensive, it will create valuable waterfront land. This is the argument used by many real estate agents in Istanbul. The promise is simple: a new waterway will create water-facing neighbourhoods and early buyers will benefit from future scarcity.

Waterfront value is not created by water alone. It depends on the quality of the water, the surrounding urban fabric, views, access, demand, prestige, management, and long-term desirability. A shipping canal carrying cargo vessels, tankers, tugboats, sediment, dredging activity, and operational infrastructure is not the same as a natural coastline, a marina town, or a historic strait.

There is a reason the Bosphorus is valuable. It is not simply a strip of water. It is geography, history, architecture, rarity, international recognition, and irreplaceable setting. An artificial canal cannot copy that. Buyers should be careful when a canal-facing apartment is presented as if it were a Bosphorus mansion in waiting. It is not.

An Industrial Canal Is Not a Lifestyle Waterfront

Canal Istanbul would connect two very different bodies of water: the Black Sea and the Sea of Marmara. The Marmara Sea already faces serious environmental pressure, including pollution, oxygen stress, wastewater issues, and mucilage outbreaks. The Black Sea and Marmara system is hydrologically complex, with different salinity levels and water movement.

Critics argue that adding a second artificial passage could alter flows, increase pollution pressure, threaten water resources, and worsen ecological stress in the Marmara Sea. Concerns include:

- Damage to Sazlıdere and Terkos water resources.

- Greater pressure on the Marmara Sea.

- Dredging, excavation soil, and long-term maintenance risk.

- Possible odour, algae, oxygen, sediment, and water-quality problems.

- More development pressure around already sensitive northern land.

A canal promoted as waterfront living would also be a major engineered water system requiring constant management. If circulation, pollution, oxygen levels, sediment, algae, or odour problems emerge, the “waterfront premium” becomes a liability for investors.

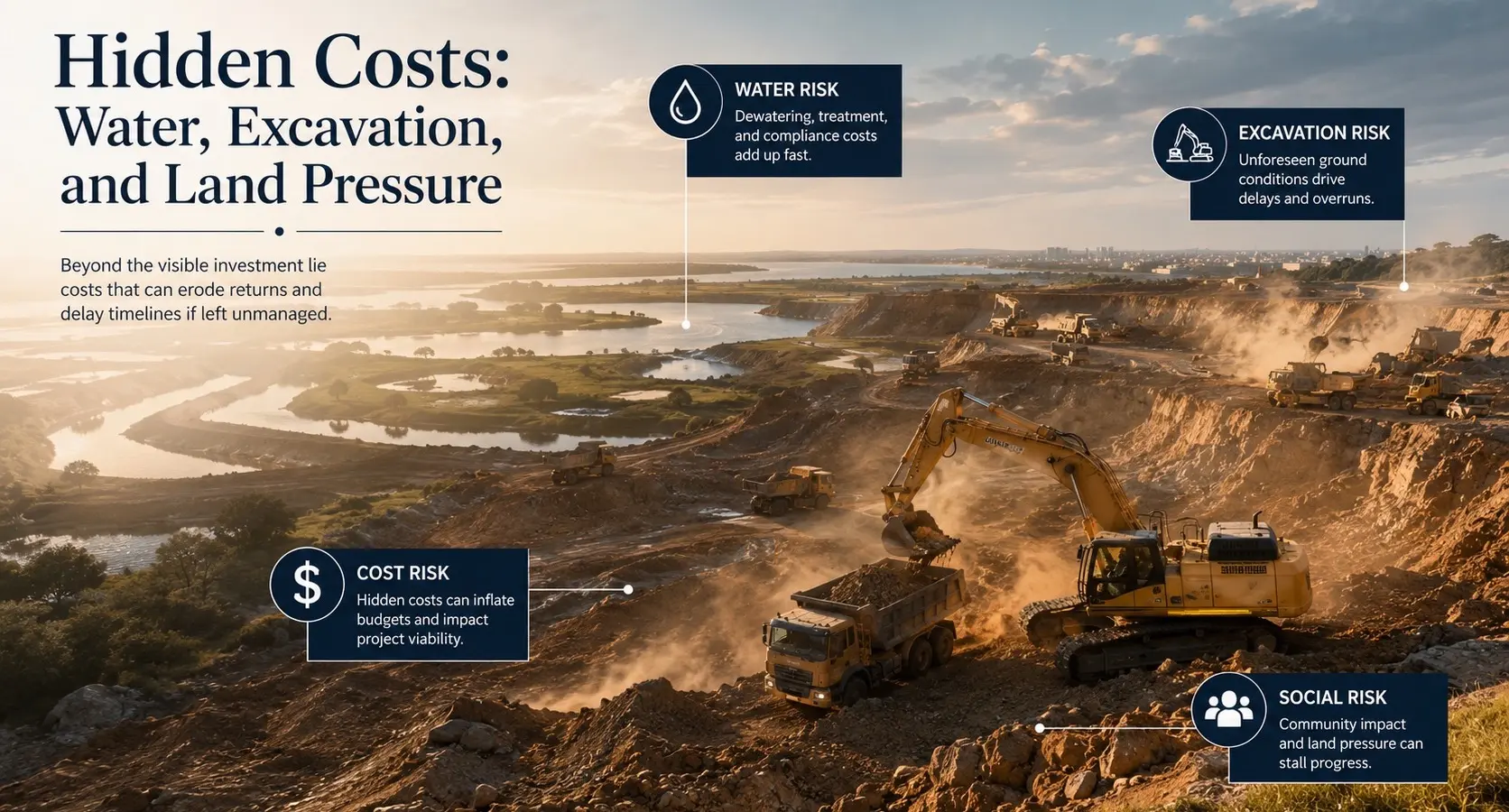

Hidden Costs: Water, Excavation, and Land Pressure

Canal Istanbul is not just a waterway. It would cut through sensitive parts of Istanbul’s northern environmental system, including areas connected to Sazlıdere, Terkos, agriculture, wetlands, and long-term water security.

The risks affect how Istanbul grows, where pressure moves, and who carries the cost if the project creates environmental or planning problems:

- Water Risk: The route passes through areas linked to Istanbul’s water resources. Any damage to basins, natural drainage, or surrounding land could create long-term pressure for a city that already faces serious water demand.

- Excavation Risk: Canal Istanbul would involve around 1.17 billion cubic metres of excavation. This means moving enormous amounts of earth, stabilising canal banks, managing water inflow, building crossings, and dealing with dredging and fill areas.

- Cost Risk: Every major engineering task adds uncertainty. Delays raise financing costs. Environmental mitigation adds expense. Legal challenges slow delivery. A canal that looks simple on a sales map becomes far more complex in reality.

- Social Risk: New infrastructure often opens land to faster development than originally promised. Roads, logistics sites, housing, and speculation can push Istanbul further into agricultural land, water basins, and ecological areas.

This is why the Canal Istanbul debate is not only about ships. It is also about land. Who owns it? Who benefits from zoning changes? Who sells early? Who buys late? Who carries the risk if the canal is delayed or never completed?

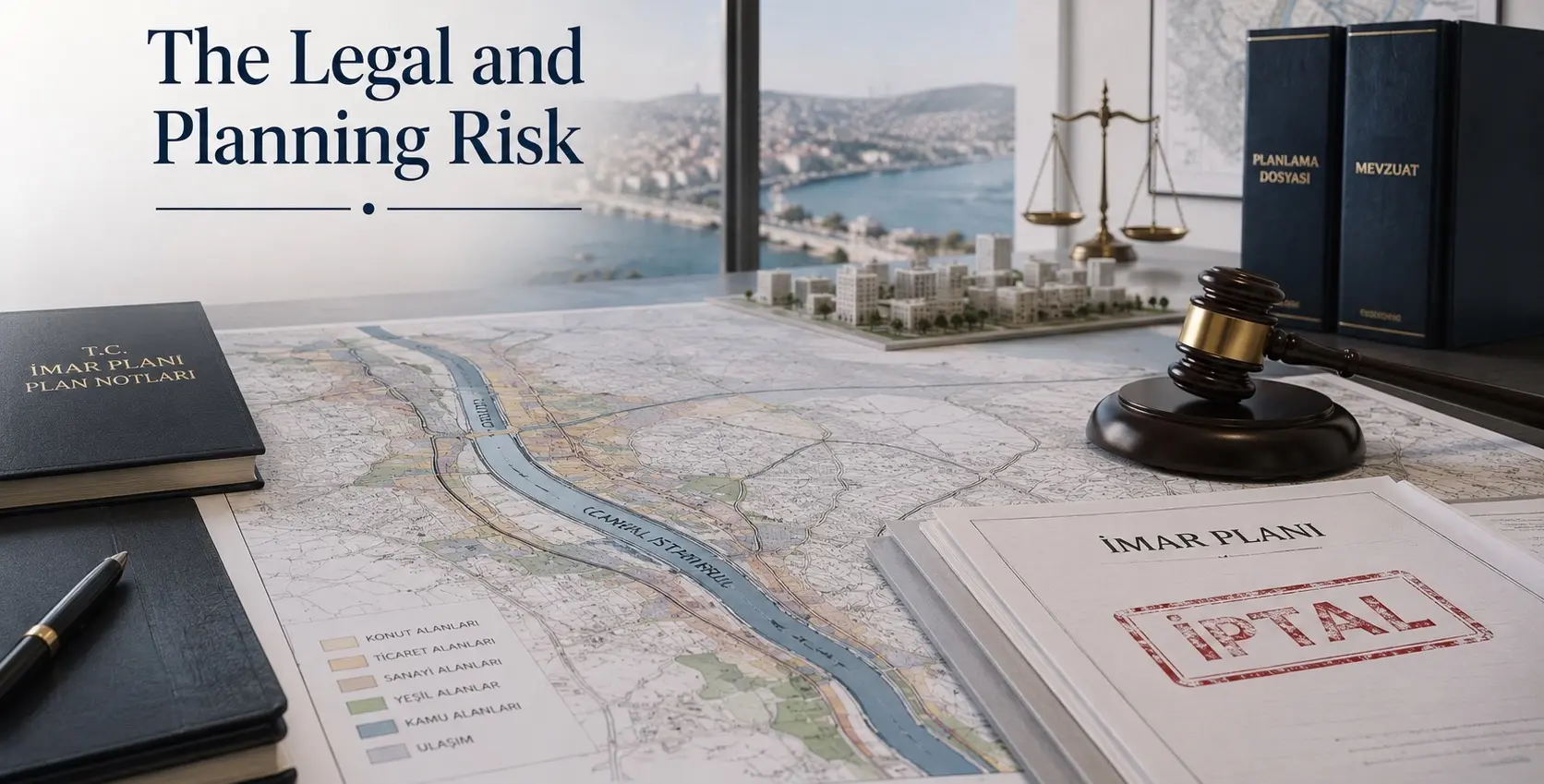

The Legal and Planning Risk

Canal Istanbul is not only controversial in public debate. It has also faced legal and planning obstacles. In 2024, Istanbul’s 11th Administrative Court cancelled zoning plans for the Canal Istanbul Yenişehir Reserve Construction Area. The court reportedly found that objections were justified and that the plan was not in line with urban planning principles and fundamentals.

That alone should make buyers cautious.

If an agent presents Canal Istanbul as if it were a normal infrastructure project moving steadily through delivery, the legal record says otherwise. A project with cancelled planning, active objections, environmental disputes, and uncertain financing cannot be sold as a guaranteed future amenity.

Current Status: Not Abandoned, Not Active

In 2025, Turkey’s transport minister said the project had not been abandoned, but also said it was not on the agenda at that time and would proceed when the right financing was found. That is not the language of an active, fully funded mega project. It is the language of a project being kept alive politically.

Many large projects remain in public discussion for years. Some are studied, revised, relaunched, or repackaged. Some survive as campaign promises. Some support land speculation long before any real construction begins.

Canal Istanbul has already lived through that cycle. It is announced. It is promoted. It is debated. It becomes quieter. Then it reappears. For a property buyer, that cycle should not be confused with delivery.

Why Some Real Estate Agents Still Sell It

The reason some agents continue to promote Canal Istanbul is simple: it creates urgency. “Buy before the canal is built” is powerful. It gives buyers a reason to act quickly. It turns undeveloped or peripheral land into a future waterfront. It allows speculative pricing to be framed as early access. But serious investors should always ask what remains if the promised event does not happen.

If a property has transport access, rental demand, nearby employment, completed infrastructure, legal Title Deed, fair pricing, and a clear resale market, then it may be worth considering. If a property is good only because Canal Istanbul might one day be built, it is speculation dressed as investment.

What Investors Should Ask Before Buying Near Canal Istanbul

Question

Why It Is Important

Is the project fully financed?

Without financing, a mega project remains political language

Are the relevant zoning plans valid and current?

Planning risk can damage resale and future development rights

Does the property work without the canal?

A sound investment should not depend on one uncertain event

Is demand based on real residents or future speculation?

Sustainable value comes from users, not only map-based selling

What infrastructure is already completed?

It means completed roads, metro access, schools, hospitals, and jobs

Is the area exposed to environmental or legal objections?

These can slow delivery, affect values, and reduce buyer confidence

Who is the likely resale buyer?

If the only buyer is another speculator, liquidity risk is high

Istanbul Does Not Need Canal Istanbul to Be Investable

The city already has genuine real estate drivers: population depth, international demand, Urban Regeneration, transport expansion, business districts, universities, hospitals, tourism, finance, and long-term housing need. Areas such as central Istanbul, the Asian side, the airport economy, and selected renewal districts can all be analysed without relying on speculative canal claims.

Canal Istanbul, by contrast, appears strongest when details are kept vague. Once the analysis becomes specific, the weaknesses become clear: uncertain financing, disputed environmental impact, legal objections, questionable toll economics, water risk, and property speculation around a project that may never arrive.

Investment Conclusion: Do Not Buy a Promise

Canal Istanbul is one of the most ambitious ideas ever proposed for Istanbul. It is also one of the least convincing when judged as a reason to invest in nearby real estate.

The shipping revenue argument is weak because the Turkish Straits do not carry the same high-value cargo profile as the world’s strongest toll waterways. The existing fee income is far below what would be needed to support a project of this scale. A high canal toll would face resistance unless ships had no practical alternative.

The real estate argument is also weak. An artificial shipping canal is not a second Bosphorus. It does not automatically create prestige waterfront. It brings environmental, operational, planning, and social risks that could reduce, not increase, long-term desirability.

The ecological case is unresolved. The water supply concerns are serious. The legal risk is visible. The political timing is obvious. The financing remains uncertain. For these reasons, Canal Istanbul should be treated as a political mega-project, not an investable certainty.

Advice Before Buying Near Canal Istanbul

Do not buy property because an agent tells you Canal Istanbul is coming. Buy only where the investment makes sense without it. If the canal is ever built, investors can reassess the facts then. Until that day, Canal Istanbul remains what it has been for years: a powerful political promise, a useful sales tool, and a weak basis for serious investment.

If you are considering property in Istanbul, speak to Property Turkey before making decisions based on Canal Istanbul claims. Our team can help you separate real infrastructure, completed developments, and proven investment areas from political promises and speculative sales talk. Contact us today for clear, independent guidance on where Istanbul property investment still makes genuine sense.

Cameron Deggin Founder & CEO, Property Turkey

Cameron Deggin is Founder and CEO of Property Turkey. A former finance professional and FCCA-qualified accountant, he founded the company in 2001 after recognising Turkey’s investment potential. With more than two decades analysing Turkish real estate, Cameron regularly advises international investors and is quoted by media including the Financial Times and BBC.

By:

By:

Founder & CEO, Property Turkey

Founder & CEO, Property Turkey

Bodrum

Bodrum  4

4  5

5

X

X