The key question is simple: do the goods have to physically enter Turkey?

The answer is no. In fact, for the new transit trade incentive, the opposite is true. The goods should be bought abroad and sold abroad without being brought into Turkey. The Turkish company can manage the transaction, issue invoices, arrange finance, negotiate contracts, coordinate logistics, act as intermediary, and earn the margin, but the cargo itself should remain outside Turkish customs.

That makes this reform very different from a normal import-export model. It is not designed for goods manufactured in Turkey and sold overseas. It is not designed for goods imported into Turkey, stored locally, and then re-exported. It is aimed at merchanting and intermediary income where Turkey becomes the management, invoicing, finance, and coordination base for global trade.

Put simply, what has to be in Turkey is the company and the management function, not the cargo. For the right international business, this could be a major reason to establish a Turkish company, relocate management functions to Istanbul, or consider the Istanbul Finance Center as part of a wider corporate structure.

What Changed Under Turkey’s 2026 Tax Reform?

Law No. 7582, published in the Official Gazette dated 4 June 2026 and numbered 33270, introduced a 95% corporate tax deduction for qualifying income from transit trade. For companies operating in the Istanbul Finance Center, or in certain approved industrial areas, the deduction can rise to 100%.

Transit trade is generally understood as the purchase of goods abroad and the sale of those goods abroad without bringing them into Turkey. The new deduction also covers income from intermediary activities relating to foreign-to-foreign goods transactions, provided the relevant conditions are met. In practical terms, this means:

- Outside the Istanbul Finance Center, 95% of qualifying transit trade profit can be deducted from the corporate tax base.

- Assuming Turkey’s standard 25% corporate tax rate, only 5% of the profit is taxed, creating an effective tax rate of around 1.25%.

- Inside the Istanbul Finance Center, qualifying companies may be able to deduct 100% of the relevant income, creating a true 0% corporate tax result on that qualifying transit trade profit.

- The income must be transferred to Turkey by the annual corporate tax return filing deadline.

- The buyer and seller should be outside Turkey, especially in intermediary structures.

- The transaction must be real, documented, and genuinely managed from Turkey.

Turkey has not merely reduced the tax burden for certain export activities. It has created a near-zero tax route for qualifying foreign-to-foreign goods trading managed through a Turkish company.

The Central Rule: The Goods Should Not Enter Turkey

The most misunderstood part of the incentive is the physical movement of the goods. Many investors assume that because the company is in Turkey, the products must also pass through Turkey. That is not how the transit trade incentive works.

A qualifying structure might look like this: A Turkish company buys electronics from China and sells them to a buyer in Germany. The goods are shipped directly from China to Germany. The Turkish company negotiates the purchase, manages the sale contract, issues the invoice, coordinates payment, arranges logistics, and records the profit in Turkey. The goods never enter Turkey. That is the type of commercial model the reform appears to target.

A second structure might involve intermediation. A Turkish company may arrange, coordinate, or intermediate the purchase and sale of goods between two foreign parties, while the goods move directly from one foreign country to another. Again, the key point is that the Turkish company manages the transaction from Turkey, but the goods do not cross Turkish customs.

If the goods are brought into Turkey, cleared through Turkish customs, stored in Turkey, or sold domestically, the transaction may fall outside the transit trade deduction. It may then become an import, export, warehousing, distribution, or manufacturing issue, with a different tax and customs analysis.

Transit Trade Compared with Other 2026 Incentives

Turkey’s 2026 tax package includes several different incentives, and they should not be merged together. The transit trade incentive is one part of a much wider reform agenda, but it has its own conditions.

Activity Type

Physical Movement of Goods

Main 2026 Tax Treatment

Best Suited To

Transit trade

Goods bought abroad and sold abroad without entering Turkey

95% deduction generally, 100% in the Istanbul Finance Center or certain approved industrial areas

Merchanting, commodity trade, distribution margins, foreign-to-foreign trade

Intermediation in foreign-to-foreign goods transactions

Goods remain outside Turkey while the Turkish company coordinates or intermediates the transaction

95% deduction generally, 100% in the Istanbul Finance Center or certain approved industrial areas, subject to conditions

Intermediary companies, procurement structures, trading desks, international supply chain coordinators

Qualified service centres

Services managed from Turkey for foreign group companies

95% deduction generally, 100% in the Istanbul Finance Center or certain approved industrial areas

Regional HQ, finance, procurement, management, shared service functions

Production income

Goods produced in Turkey

12.5% corporate tax rate from 2027 for qualifying production and agricultural production income

Manufacturers and producers with Turkish operations

Financial services provided from the IFC to non-residents

Extended IFC incentives, subject to separate conditions

Financial institutions and IFC participants

Is This Really a 0% Tax Regime?

It can be, but only in the right structure. For an ordinary Turkish company outside the Istanbul Finance Center, the deduction is 95%. If the company earns $1 million USD of qualifying transit trade profit, $950,000 USD may be deducted from the corporate tax base. The remaining $50,000 USD is taxed. Assuming the standard 25% corporate tax rate, the tax would be $12,500 USD. That produces an effective corporate tax rate of 1.25% on the $1 million USD profit.

Inside the Istanbul Finance Center, the deduction may be 100% for qualifying income. In that case, the same $1 million USD of qualifying transit trade profit could potentially be fully deducted from the corporate tax base, leaving no Turkish corporate tax on that qualifying income. However, three points must be kept in mind:

1 – The Company Must Actually Qualify: Having a Turkish company is not enough. For the 100% version, the company must meet the Istanbul Finance Center or approved industrial area requirements.

2 – The Income Must be Correct Type of Income: A Turkish company with several business lines should separate qualifying transit trade income from ordinary income, domestic income, service income, and other revenue.

3 – Large Multinational Groups: Need to consider Pillar Two global minimum tax rules. For multinational groups within the global minimum tax framework, a low Turkish tax outcome may not always create a permanent group-level saving if another jurisdiction can collect top-up tax. Pillar Two is designed around a 15% global minimum effective tax rate for in-scope multinational groups, so a large group benefiting from a 0% or near-zero Turkish result may still face top-up tax elsewhere in the group structure. For mid-sized trading groups below the Pillar Two threshold, the incentive could be much cleaner. For large multinational groups, the structure still needs careful modelling.

What Must be Managed in Turkey?

The reform should not be treated as a shell-company opportunity. A Turkish company that only issues invoices, while all real decision-making happens elsewhere, could be vulnerable in a tax review. A robust structure should show that meaningful commercial functions take place in Turkey. Depending on the business, this may include:

- Contract negotiation and approval from Turkey.

- Supplier and buyer management from the Turkish office.

- Logistics coordination and freight management.

- Financing, payment, treasury, or banking coordination.

- Risk management, insurance, and credit control.

- Commercial staff, directors, or decision-makers based in Turkey.

- Board minutes, contracts, invoices, and correspondence that support this.

- Accounting records that clearly separate qualifying and non-qualifying income.

- Evidence that the income was transferred to Turkey before the relevant tax filing deadline.

This is where tax planning becomes important. The legal benefit is powerful, but it needs operational substance. Turkey should be more than the invoice address. It should be where the trading function is genuinely directed and managed.

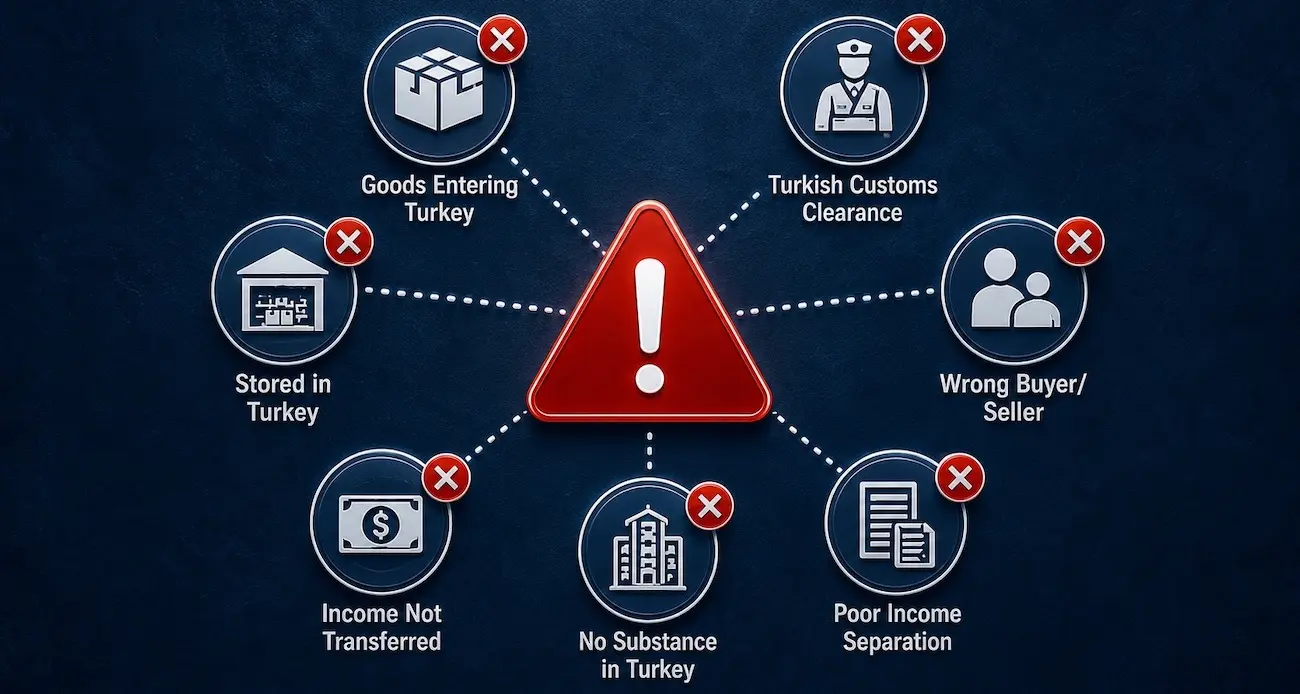

What Could Disqualify the Income?

The biggest risk is misunderstanding what transit trade means. Bringing goods into Turkey may move the activity away from the new incentive. Possible risk points include:

- Goods being imported into Turkey.

- Goods being cleared through Turkish customs for domestic circulation.

- Goods being stored in Turkey before sale.

- A Turkish buyer or seller being involved in the wrong part of the transaction.

- Income not being transferred to Turkey by the required deadline.

- Contracts showing that real management is outside Turkey.

- Poor separation between qualifying transit trade income and ordinary Turkish income.

- Using the structure only for tax reasons, without commercial substance.

- Assuming that a bonded warehouse in Turkey automatically qualifies.

- Treating a Turkish company as a simple invoicing shell.

In simple terms, the cleanest version to qualify, is this: the Turkish company manages the deal, but the cargo moves from one foreign country to another foreign country without touching Turkey.

Why Is This Important for Foreign Investors?

Turkey is already an attractive base for companies trading between Europe, the Middle East, Central Asia, Africa, and Asia. Istanbul offers strong banking access, a large professional services market, international flight connections, experienced logistics providers, and a deep pool of commercial talent.

The 2026 transit trade reform adds a tax reason to that business case. A foreign trading group may now ask whether it makes sense to locate merchanting, procurement, or regional management activity in Turkey. The opportunity may be important for:

- Commodity traders.

- Electronics and consumer goods distributors.

- Textile, furniture, and household goods trading companies.

- Industrial equipment suppliers.

- Food and agricultural commodity traders.

- Regional procurement companies.

- Family-owned trading groups.

- Businesses currently using higher-tax jurisdictions for foreign-to-foreign trade.

- Companies considering Istanbul as a regional headquarters location.

For these groups, the incentive can be viewed in two ways. Outside the Istanbul Finance Center, it may reduce the effective tax burden on qualifying income to around 1.25%. Inside the Istanbul Finance Center, it may create a 0% result for the right type of income, subject to full compliance.

Tax Planning Points Before Using the Incentive

The transit trade incentive is attractive, but it should be planned properly before a company starts routing income through Turkey. A sensible review should cover the following questions:

1. Does the business model qualify? Are the goods bought abroad and sold abroad without entering Turkey? Are the buyer and seller outside Turkey? Is the Turkish company acting as principal, intermediary, or coordinator?

2. Where is the income earned? The company should identify the exact profit margin that relates to qualifying transit trade and separate it from other income.

3. Where is the real management? Directors, staff, contracts, finance, and logistics decisions should support the position that the trading activity is genuinely managed from Turkey.

4. Can the income be transferred to Turkey on time? Cash flow planning is essential because the deduction depends on the income being brought into Turkey by the corporate tax return deadline.

5. Should the company operate inside the Istanbul Finance Center? The difference between a 95% deduction and a 100% deduction could be material for high-margin trading groups.

6. Does Pillar Two apply? Large multinational groups should model whether the Turkish tax saving will be affected by global minimum tax rules. For in-scope groups, the global minimum tax framework may reduce or remove the group-level benefit of a near-zero local tax result.

7. Are customs, VAT, and transfer pricing risks controlled? Even if the corporate tax incentive applies, the wider structure must still be checked for customs, VAT, withholding tax, transfer pricing, treaty, and accounting consequences.

8. Is there enough evidence of substance in Turkey? Contracts, board approvals, commercial correspondence, staff responsibilities, bank records, accounting records, logistics decisions, and risk control should all support the position that the income is managed from Turkey.

Speak to Property Turkey About Structuring Your Move

Turkey’s 2026 tax reforms have created a new planning opportunity for international investors, business owners, trading companies, and families considering Turkey as a long-term base. The transit trade incentive is important because it may allow qualifying companies to manage foreign-to-foreign goods transactions from Turkey with a much lower corporate tax burden.

However, the structure has to be right from the start. The goods movement, buyer and seller location, company setup, management substance, banking, accounting records, income transfer deadline, Istanbul Finance Center status, and wider tax position all need to be reviewed before relying on the deduction.

Important: This article is for general information only and should not be treated as tax, legal, or financial advice. Any structure involving transit trade, the Istanbul Finance Center, Turkish tax residency, company formation, foreign-source income, or Turkish Citizenship by Investment should be reviewed by qualified Turkish tax and legal professionals before action is taken.

Cameron Deggin Founder & CEO, Property Turkey

Cameron Deggin is Founder and CEO of Property Turkey. A former finance professional and FCCA-qualified accountant, he founded the company in 2001 after recognising Turkey’s investment potential. With more than two decades analysing Turkish real estate, Cameron regularly advises international investors and is quoted by media including the Financial Times and BBC.

By:

By:

Founder & CEO, Property Turkey

Founder & CEO, Property Turkey

Bodrum

Bodrum  4

4  5

5

X

X